January

January 29, 2008

Alabama Governor Bob Riley has recently played a huge role in lobbying FERC on behalf of Lake Martin’s water level. He is also Alabama’s most visible […]

January 16, 2008

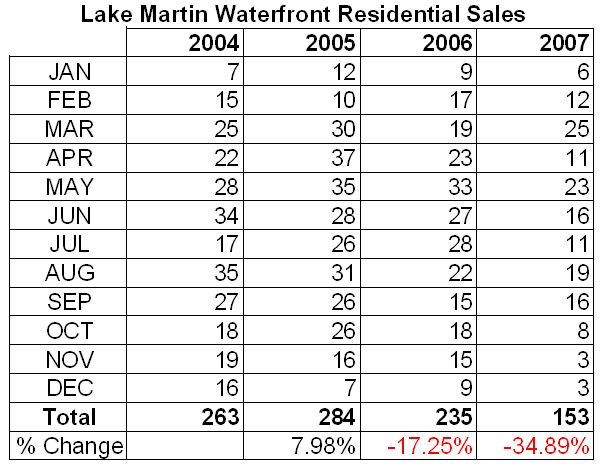

The Lake Martin real estate market suffered a major slowdown in 2007 for a variety of reasons. I dug through the sales results in the Lake […]

January 11, 2008

Trillium, one of Russell Lands’ more mature Lake Martin developments, is located just west of Kowaliga Marina. Along with Willow Point and The Ridge, Trillium has some of […]

January 6, 2008

The Lake Martin real estate market has not really felt a direct effect of the mortgage meltdown yet. Sure, the subprime fiasco has caused conventional and jumbo […]